Summary

BA Labs proposes holding back from onboarding Morpho Keyrock USDC v2 vault as an ARK to the LR USDC fleet on Mainnet at this point, due to recursive collateral risk exposure of assets listed in the vault, and outlined in detail below. This goes in line with the previous cap reductions of ARKs that have exposure to Resevoir’s rUSD, as seen here. We’ll be monitoring the collateral structure, and, in case of reduced risk, propose lifting the caps accordingly.

Risk Assessment

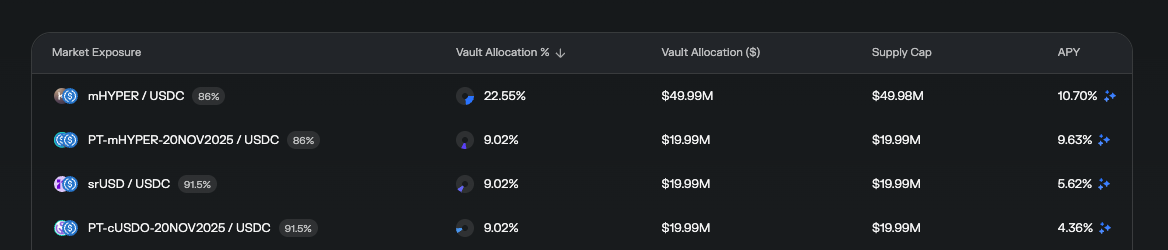

We reviewed the vault Morpho Keyrock USDC v2 as a potential addition to the LR Fleet Mainnet USDC. While the strategy leverages Morpho’s new v2 infrastructure, we note that the vault is very small in size compared to other arks in this fleet and supplies 100% of its liquidity to Morpho Keyrock USDC v1 at the moment of writing this, which in turn allocates over 60% of its assets to yield-bearing assets such as rUSD, yUSD, mHYPER and others, as seen below.

After looking at the collateral structure of those assets, we identified significant recursive collateral risk, with the main points outlined below:

Reservoir protocol’s (s)rUSD

Proof of reserves of Reservoir protocol show $535m in TVL, with the backing including a couple of Morpho v1 vaults that lend majority of USDC liquidity to the srUSD/USDC markets.

Notable exposure is through Smokehouse USDC Morpho vault which allocates >50% of liquidity (roughly $150m) to srUSD/USDC market on Morpho while Reservoir deposits ~$168m into this vault at the time of writing this.

Similar setup is currently done via Stakehouse rUSD vault on Morpho, having slightly less overall exposure to Reservoir’s srUSD token with 45% allocation (~$43m), although still deemed significant from risk perspective, with the near 100% of TVL coming from the protocol itself with around $93m.

With that said, including other vaults with lower TVL’s although with similar allocations, it shows the reserves of rUSD token are >50% in Morpho vaults receipt tokens that are collateralized by (s)rUSD itself, implying significant possibility of recursive unwinding, potentially putting pressure on redemptions and/or asset’s market price.

Hyperithm’s mHYPER

As we’re unable to identify full reserves breakdown of mHYPER token, due to simple lack of collateral transparency, we do find it concerning, similarly to the above case with rUSD, that Hyperithm curates its own Morpho USDC vaults (vault 1, vault 2) by allocating 22% of liquidity to mHYPER/USDC market (~$50m), with other allocations including PT-mHYPER tokens, srUSD/USDC, as well as yUSD which is backed by mHYPER token itself (more details in the yUSD section below).

YieldFi’s yUSD

As yUSD also accounts for significant collateral composition of the Morpho Keyrock v1 vault (and consequently v2 vault), we want to identify similar recursive patterns (and thus risks) involved via couple of Morpho vaults, including the Alpha USDC Core vault having >35% (~$20m) allocated to yUSD/USDC market with the biggest supplier being the address stated as the one representing over 77% of the uUSD balance sheet, and Clearstar’s USDC Reactor vault having >50% liquidity (~$13m) allocated to yUSD/USDC market with the address mentioned above being biggest vault depositor.

Furthermore, we believe it’s worth noting that rUSD and mHYPER are also part of the yUSD collateralization.

Therefore, we recommend refraining for now from listing it until its collateral base diversifies and the dependency on its own v1 and underlying assets is reduced.